Paying Back Student Loans: The Good, The Bad, and… The Easy?

If you’ve graduated in the last several years, you are probably aware of the student loan debt crisis. Each year, throngs of students walk across stages to receive diplomas, but few are walking into full-time jobs during the workweek. As a result, these graduates have a lot of student loan debt and very little income to pay it back. But, they shouldn’t give up. We’re going to discuss the “good” features of student loan repayment (use these to your advantage!), the “bad” traps to watch out for, and we will tell you how paying back student loans can be easy if you do a few things right!

The Good

Trying to pay back student loan debt? You aren’t alone, and that’s a good thing. There are several basic programs and features that have been put in place to help you pay back your student loans. Here are several strategies you can use:

The grace period

Students with federal loans, such as the Stafford and Perkins Loans, will have a “grace period” between graduation and when loan repayment begins:

- Stafford Loans: Six-month grace period

- Perkins Loans: Nine-month grace period

Students should take advantage of this time to build savings that they can put toward their student loan debt. If you aren’t able to secure a full-time job right away, at least look for side jobs and part-time jobs. Every little bit you can put aside now will be helpful when you start having monthly payments on your loans.

*Also, keep in mind that interest accrues during the grace period. If you are able, it is a good idea to pay the interest off during the grace period.

Set up automatic drafts from your bank account

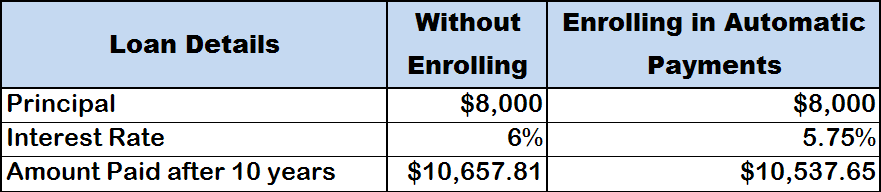

Many student loan servicers allow you to enroll in an automatic drafting system. This means that the monthly payment (or another amount you choose) is taken from your bank account each month. The benefit: Many services offer an interest reduction on your student loans (usually .25%) if you enroll in this service. Here’s an example of the interest that can be saved:

While this won’t save you a TON of money (in this example it’s only about $120 over a ten-year period), it does add up, especially if you can do this for multiple loans. Of course, this also helps to ensure that you won’t miss a payment. Just be sure you keep enough funds in your account (you don’t want to overdraft) and to notify your student loan servicer if your bank account or card number changes.

Tax Breaks

Even if you just graduated, you might be eligible for a tax break for your last year of college. Here are two tax credits and brief explanations:

- The American Opportunity Tax Credit: This is a tax credit of up to $2,500 of the cost of tuition, fees and course materials paid during the taxable year. Also, 40% of the credit (up to $1,000) is refundable. This means you can get it even if you owe no tax. (Source: IRS)

- The Lifetime Learning Credit: This is a credit up to $2,000 for “tuition and fees required for enrollment or attendance (including amounts required to be paid to the institution for course-related books, supplies, and equipment)” Source: IRS

Student Loan Interest Deduction

Near tax time, each of your student loan servicers will send you a 1098E form if you have paid interest on your accounts with them (Note, according to the IRS, the servicer is only required to provide this form if interest paid is greater than $600). This shows how much interest you have paid toward your student loan debt in a given year. You can deduct up to $2500 in student loan interest when you file your taxes.

If you don’t receive a form, log in to your online account or call the servicer’s customer service.

Student Loan Repayment Plans and Forgiveness Options

There are many student loan repayment plans, such as:

- Income-based repayment plans

- Pay as you earn plans

- Occupation-based forgiveness programs

It can sometimes be challenging or confusing to find out if you are eligible for these programs. Clearpoint’s student loan counseling can help. Read more about our student loan counseling program, and talk to a counselor to learn if you may potentially qualify for these programs.

The Bad

There are some traps to look out for when paying back student loans. These will make your loan repayment far more challenging.

Other Debt

Other debt will make paying back student loans more difficult. Hear what Bruce McClary has to say:

If you have credit card debt or car payments, your student loan repayment will be a little trickier. This is because the interest rate on your credit cards and vehicle are likely higher than the rates on your student loans (although keep in mind that private student loans have much higher interest rates than federal student loans). Because these rates are higher, you need to pay them first. This will, however, slow down your ability to pay back student loan debt.

You will need to budget carefully so that you can make the minimum payments to your student loans while also maximizing contributions to your other debt. You want to put money toward the highest interest accounts first. Prioritize your debts by interest rates, like this:

Recreational Spending

Recreational spending can create problems when you are paying back student loan debt, because it minimizes the amount you can put toward your loans. Going to expensive concerts on the weekends, going out to eat multiple times a week, etc. can create some real problems.

Plan for fun events in advance so that you can save for them. Don’t plan too many, either. You should reward yourself along the way while you pay your student loans, but don’t overdo it. Consider the following example:

Johnny goes out to east three nights a week. In a year, he spends $1560 on dinners out. He’s really struggling to pay off his student loan debt, but he needs food to survive, right?

Jenny goes out to eat one night each week. On the other two nights that Johnny is out, she makes meals from our $5.55 cookbook.

She only spends $982.8 per year on food for these three nights of the week. She has an extra $577.2 to pay back student loan debt over the course of the year. Over the course of a 10-year student loan repayment plan, she will have $5,772 more to put toward her student loans, just because she decided to eat in!

This is a good example of how you can do fun things, and by not overdoing them, you can still have ample funds to pay off your loans.

Missing a Payment

When you miss a student loan payment, the loan becomes delinquent. If the loan remains delinquent for 90 days, your student loan servicer will report it to the credit bureaus, and your credit score will take a hit (making it more difficult to get good terms on future loans, to get a job, to rent an apartment, etc.). Depending on the type of loan, it will go into default after 270 or 330 days without a payment.

From here:

- You lose federal student aid eligibility.

- You will begin to receive calls from debt collection agencies.

- Your tax refund and wages may be withheld.

- Your credit report and score can be damaged for years.

If you are struggling with the “bad” side of student loan repayment, Clearpoint can help. A student loan counseling session may be just what you need!

The Easy

Most people don’t think of anything “easy” when they think of student loans, but we challenge you to think differently. If you can land a full-time job and avoid other debt after college, you might be debt-free faster than you think. In fact, you might even think paying back student loans is “easy.” Here’s why:

The average salary after graduation is $44,455 (keep in mind that this depends on where you live and your field of study—expect less if you majored in liberal arts). The average student loan debt is about $26,600. Now, over the course of five years, someone with the average salary for college graduates would make about $222,275 (not including any raises), and the $26,600 in debt (not including interest) would only represent 12% of the income over this five year period.

In this scenario, paying back student loans in full would be fairly easy to do in less than five years. The debt-to-income ratio in this example is 12%, and we usually tell people that anything under 15% is manageable. If you were able to save on other costs along the way like housing (living with Mom and Dad is “in” right now) you could probably accelerate the repayment even more. In fact, it could be pretty easy to pay off all your student loan debt in about two years. It really comes down to smart money management and a goal-oriented perspective. If this sounds like something you are interested, check out our post on the best way to pay off student loans which covers this strategy in more detail.

We know that paying back student loans won’t be easy for most people, especially if you have difficulty finding full-time work. That’s why we want you to understand that you are not alone. Clearpoint counselors will review your student loans along with the rest of your financial situation. We will help you discover the options that are best for you. Go ahead, give us a call at 1-800-675-7601 or visit us here.

Christopher

Collection agency..tg has started garnishing my wages 15% each week..I am soul provider for a family of 5…I am in financial hardship.I have applied for a hearing which they said it will take 2 months to consider a monthly payment with a interest fee up to 25%. Please help me.Any suggestions??

Thomas Bright

sorry to hear about this situation! My best advice is to find opportunities to cut spending in your household each month. Maybe it’s cable, cell phones, gym memberships, etc. You will really want to cut the fat while you continue through this process. From there, I would get the best legal advice you can on the matter.

rquinones

This blog says, “Students with federal loans, such as the Stafford and Perkins Loans, will have a “grace period” between graduation and when loan repayment begins…” Regardless, my student loan’s grace period with ACS Education started when I started my psychology internship in Fall/2011. I finished my Ph.D. on Summer/2013 and graduate on November/2013. Regardless, they say my grace period started when I began my one year internship on Fall/2011. Therefore, their representatives say I should have been paying since February/2012. I have not paid a cent because I was still receiving student loans to pay for school. In psychology you only make a one year internship and a dissertation (you do not get paid while doing your dissertation work). How can they be charging me student loans since Feb/2012 if I was still paying tuition with student loans? I stopped requesting these (loans) in Summer/2013 because that is when I finished my Ph.D. program. They have been calling me to charge me more money and they just say it doesn’t matter. They say that I had to start paying when I started my internship, not when I finished my graduate program. Can anyone help me out?

Thomas Bright

Hey there,

sorry to hear about that happening to you. I’m guessing this was for a federal loan? Looking back, it seems like maybe you could have enrolled in deferment with your loan servicer, on the understanding that you were going through the internship. Or, if you were actually enrolled as student, you could have gotten deferment based on that. It sounds like you attempted this but they didn’t allow it. My best advice would be to contact the loan company and continue to explain your situation and see what can be done.

I don’t think avoiding payments is a good idea, because the loan could go into default, damage your credit score, and leave you with little recourse. Instead, talk to them about a hardship program or potentially looking at some way to retroactively apply the deferment (assuming you can prove that you met the conditions).

Lastly, you can file a complaint with the Consumer Financial Protection Bureau, and they may be able to help. Here is the link.